Get a research report by report ID

curl --request GET \

--url https://api.messari.io/research/v1/reports/{reportId} \

--header 'X-Messari-API-Key: <api-key>'import requests

url = "https://api.messari.io/research/v1/reports/{reportId}"

headers = {"X-Messari-API-Key": "<api-key>"}

response = requests.get(url, headers=headers)

print(response.text)const options = {method: 'GET', headers: {'X-Messari-API-Key': '<api-key>'}};

fetch('https://api.messari.io/research/v1/reports/{reportId}', options)

.then(res => res.json())

.then(res => console.log(res))

.catch(err => console.error(err));<?php

$curl = curl_init();

curl_setopt_array($curl, [

CURLOPT_URL => "https://api.messari.io/research/v1/reports/{reportId}",

CURLOPT_RETURNTRANSFER => true,

CURLOPT_ENCODING => "",

CURLOPT_MAXREDIRS => 10,

CURLOPT_TIMEOUT => 30,

CURLOPT_HTTP_VERSION => CURL_HTTP_VERSION_1_1,

CURLOPT_CUSTOMREQUEST => "GET",

CURLOPT_HTTPHEADER => [

"X-Messari-API-Key: <api-key>"

],

]);

$response = curl_exec($curl);

$err = curl_error($curl);

curl_close($curl);

if ($err) {

echo "cURL Error #:" . $err;

} else {

echo $response;

}package main

import (

"fmt"

"net/http"

"io"

)

func main() {

url := "https://api.messari.io/research/v1/reports/{reportId}"

req, _ := http.NewRequest("GET", url, nil)

req.Header.Add("X-Messari-API-Key", "<api-key>")

res, _ := http.DefaultClient.Do(req)

defer res.Body.Close()

body, _ := io.ReadAll(res.Body)

fmt.Println(string(body))

}HttpResponse<String> response = Unirest.get("https://api.messari.io/research/v1/reports/{reportId}")

.header("X-Messari-API-Key", "<api-key>")

.asString();require 'uri'

require 'net/http'

url = URI("https://api.messari.io/research/v1/reports/{reportId}")

http = Net::HTTP.new(url.host, url.port)

http.use_ssl = true

request = Net::HTTP::Get.new(url)

request["X-Messari-API-Key"] = '<api-key>'

response = http.request(request)

puts response.read_body{

"error": null,

"data": {

"id": "2af98e9e-1c9a-4e31-80be-38e8c1211990",

"createdAt": "2026-03-25T22:43:10Z",

"updatedAt": "2026-03-26T18:17:50Z",

"assetIds": [

"818de6bf-5bb6-42c6-874c-2fb2da81a5b5",

"95111d4e-a862-41e1-829f-d661e1b8f658",

"f8852d39-3261-4345-871e-54d533918dc2",

"99b6a5f4-2200-4098-82fd-53d091bdee70"

],

"assets": [

{

"id": "f8852d39-3261-4345-871e-54d533918dc2",

"name": "Opinion",

"symbol": "opn",

"slug": "opinion"

},

{

"id": "95111d4e-a862-41e1-829f-d661e1b8f658",

"name": "Kalshi",

"symbol": "KALSHI",

"slug": "kalshi"

},

{

"id": "818de6bf-5bb6-42c6-874c-2fb2da81a5b5",

"name": "Polymarket",

"symbol": "POLY",

"slug": "polymarket"

},

{

"id": "99b6a5f4-2200-4098-82fd-53d091bdee70",

"name": "Hyperliquid",

"symbol": "HYPE",

"slug": "hyperliquid"

}

],

"authors": [

{

"id": "ecaf52b1-16eb-4322-bf02-886bea2c5b06",

"name": "Austin Weiler",

"image": "https://cdn.sanity.io/images/2bt0j8lu/production/d70ad0cd21c781575a4fc129c8b634ae0ddd2432-2283x2283.jpg?w=100",

"linkedinUrl": ""

}

],

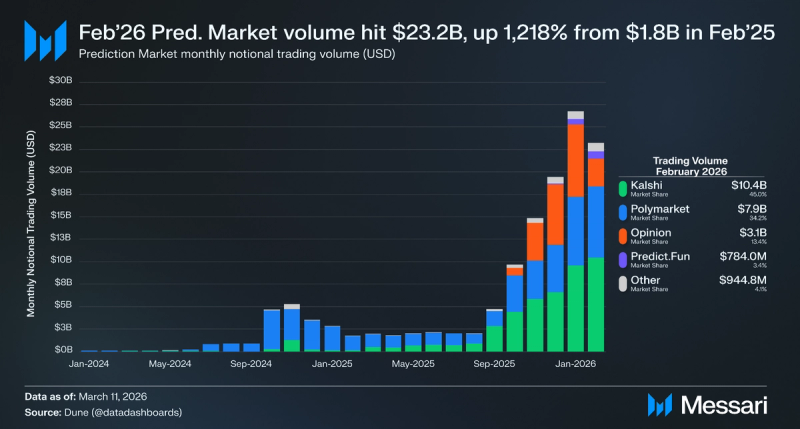

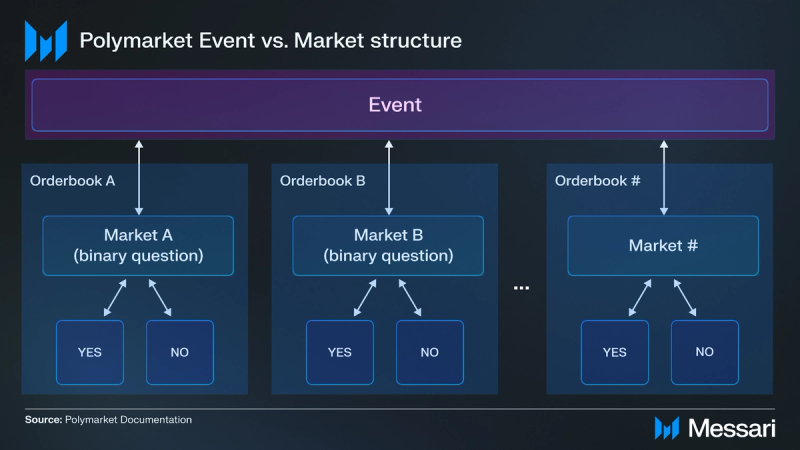

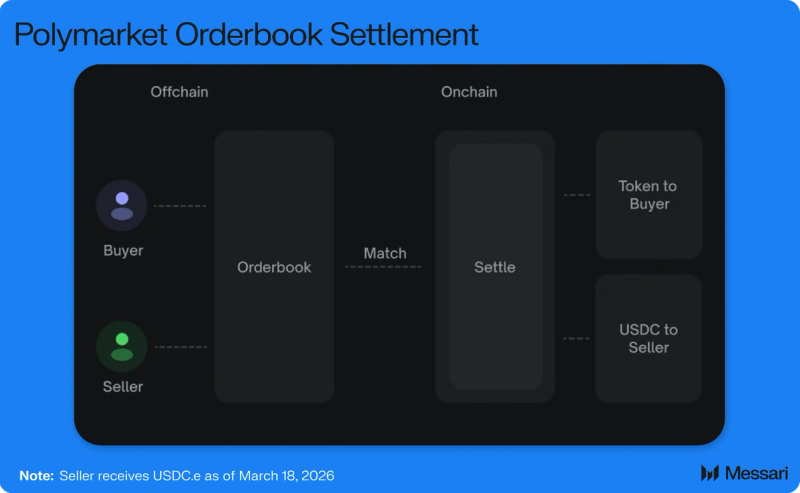

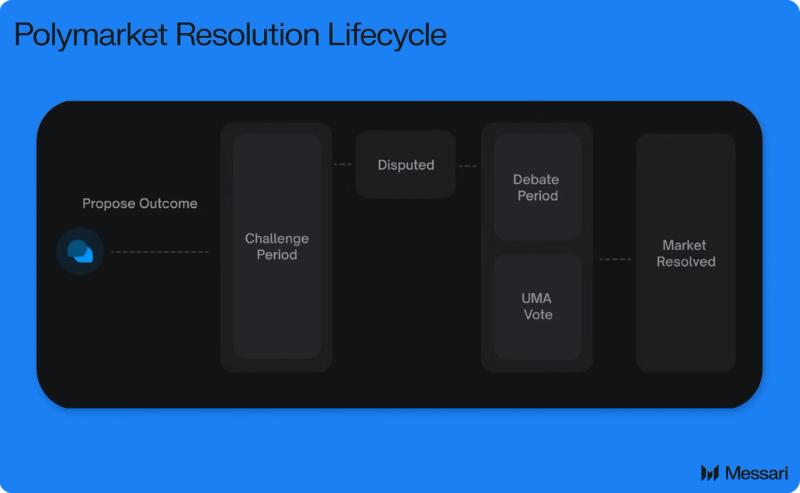

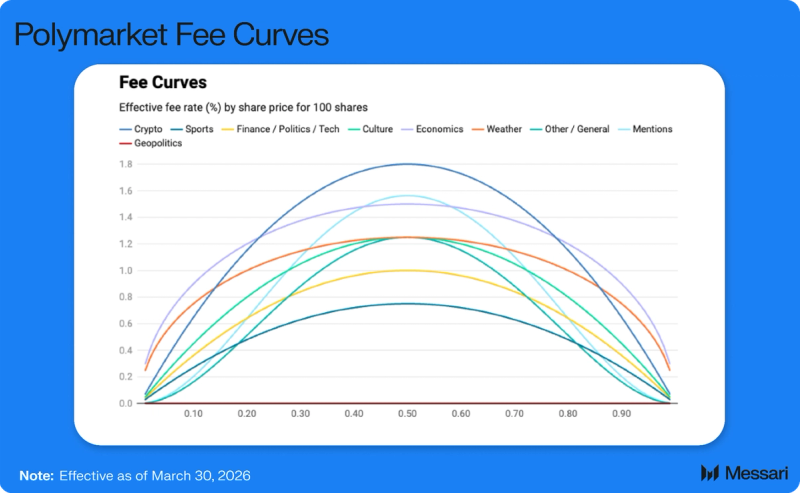

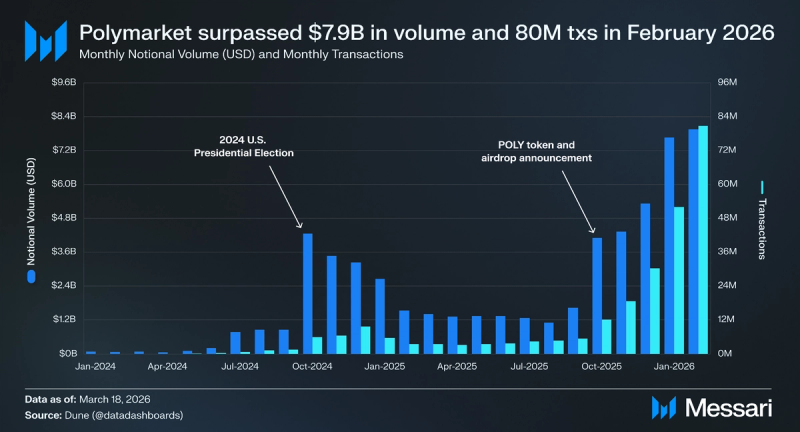

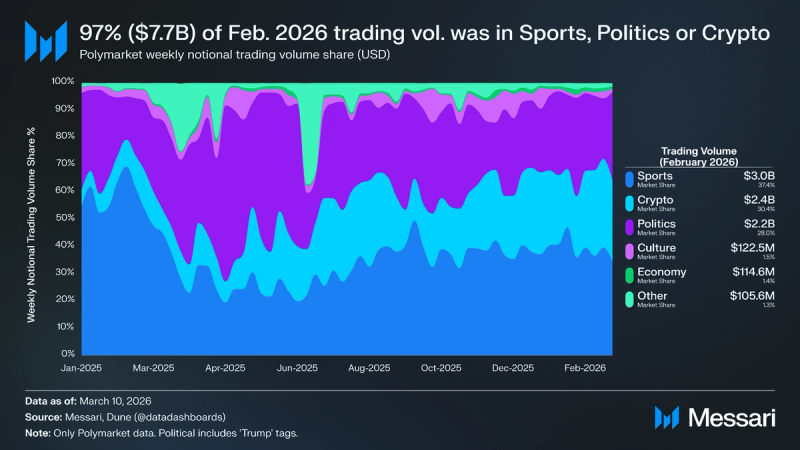

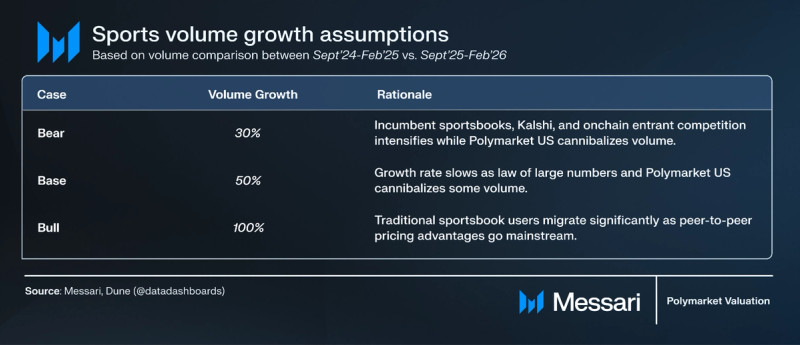

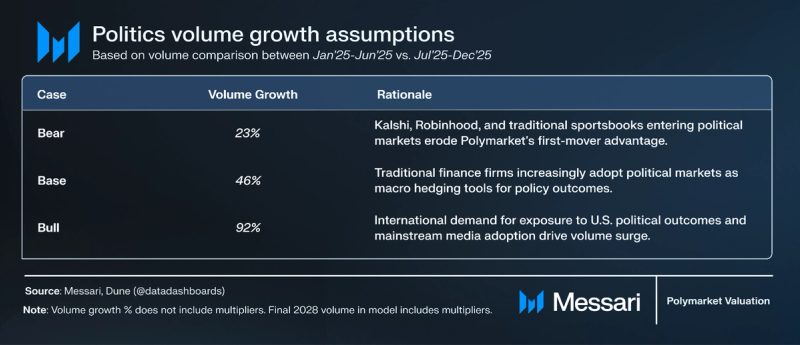

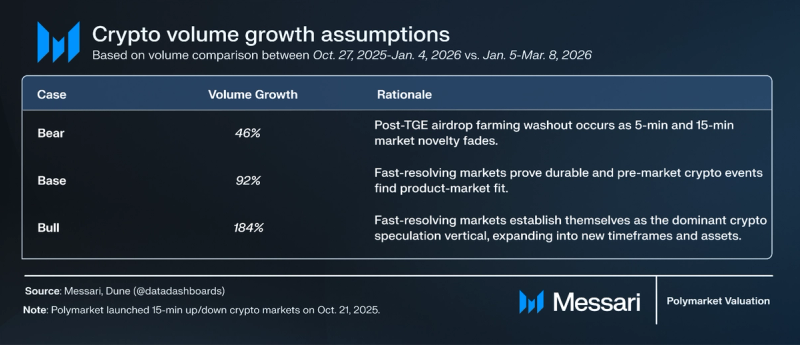

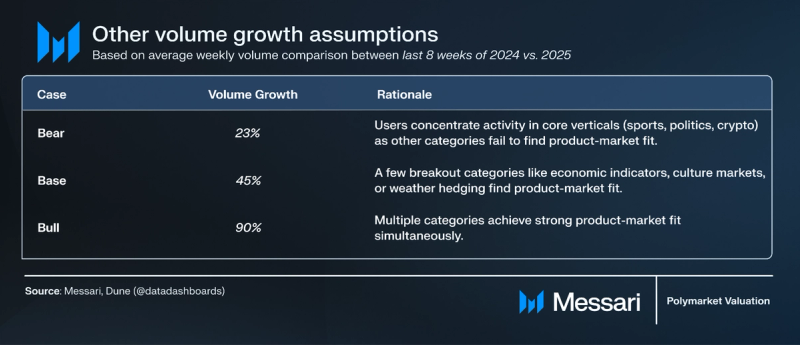

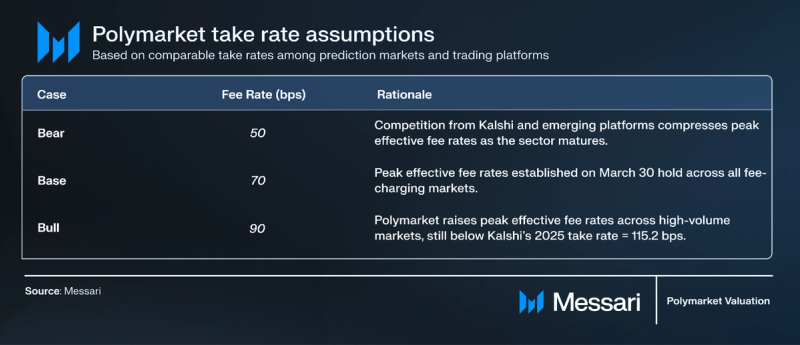

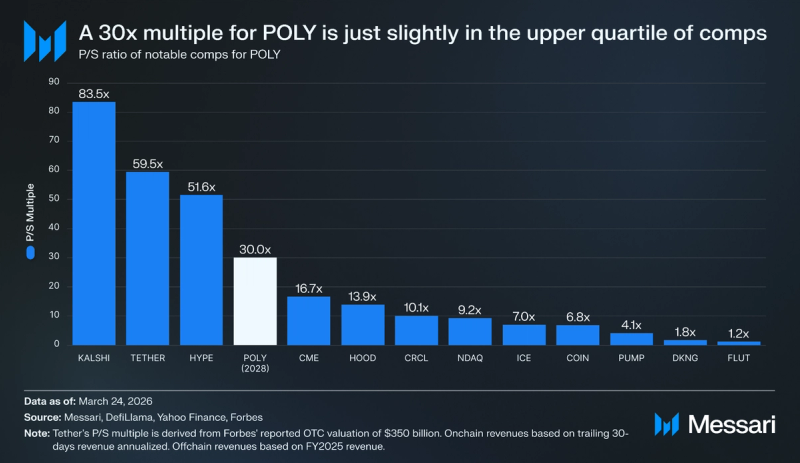

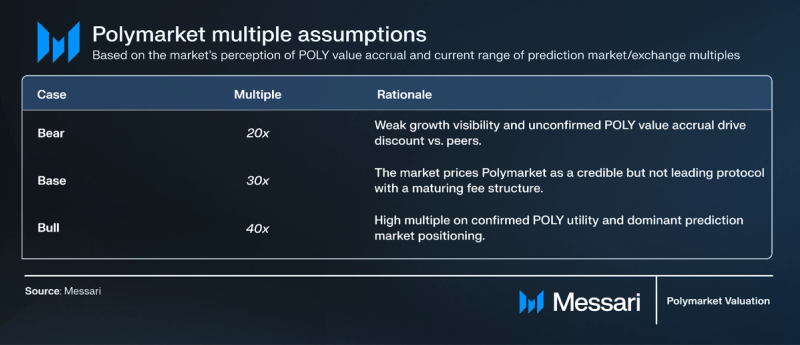

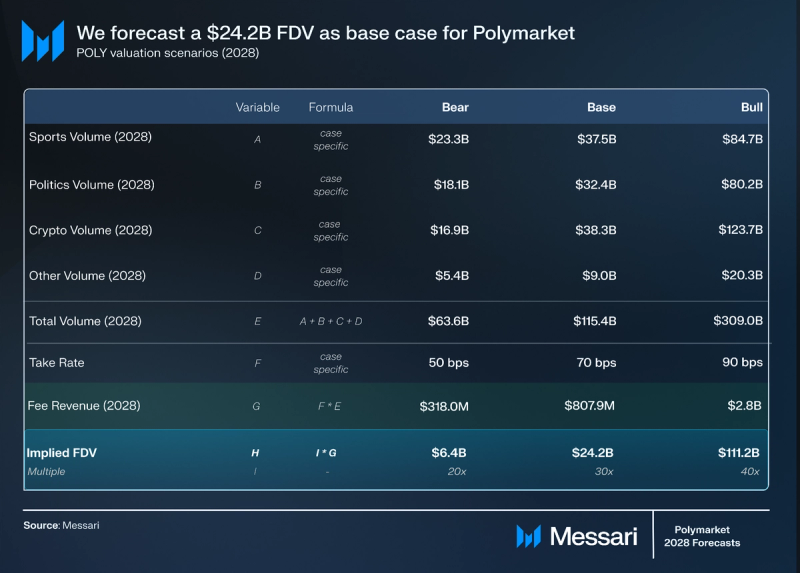

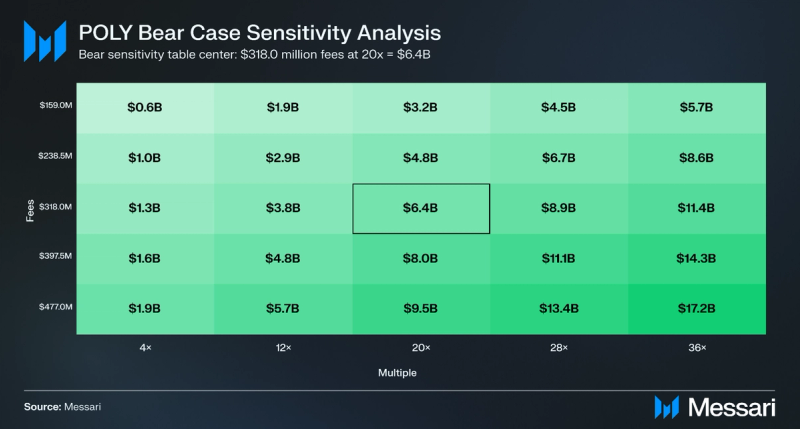

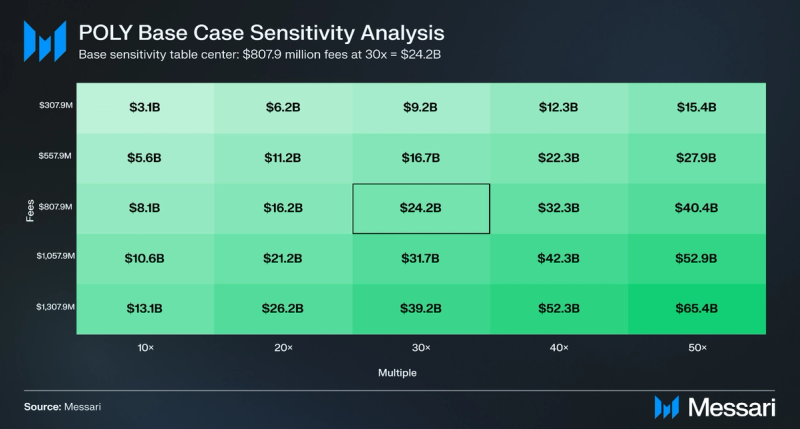

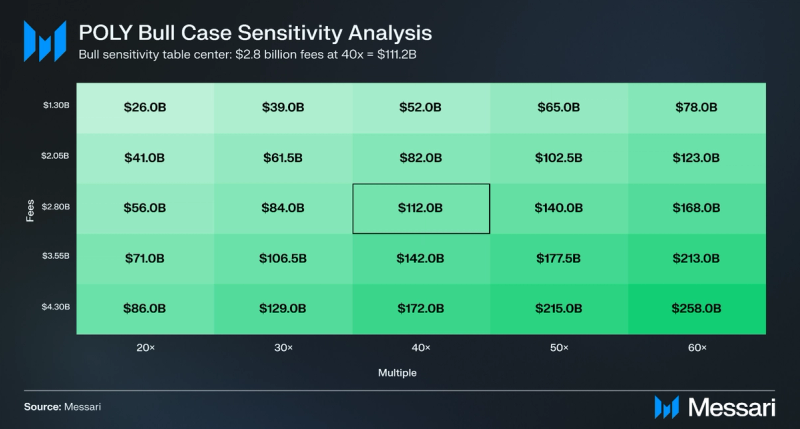

"content": "## Key Insights\n\n* **Polymarket is one of the two largest prediction markets. From** **September 2025 to February 2026, it generated $31.0 billion in volume, a 31% share**.\n* On March 7, Polymarket was reportedly seeking a $20 billion fully diluted valuation (FDV) in its next funding round, with a POLY token and airdrop confirmed in October 2025**. The central question is whether a $20 billion FDV reflects reasonable expectations for future fee generation, or if the market is mispricing the opportunity.**\n* Our valuation forecasts 2028 FDV based on volume projections across sports, politics, crypto, and other market categories, take rates, and fee multiples.\n* On **March 30, Polymarket launches taker fees on nearly all markets.** How volume responds to taker fees, increased competition, and post-airdrop volume retention will determine whether our assumptions hold.\n\n**Valuation Model:** The full valuation model, including assumptions and scenario sensitivities, is available [here](https://docs.google.com/spreadsheets/d/1JpRHkS--eHIii_P-PhsM1nrOJtfi56Qmg17qO6J9Mqk/edit?usp=sharing).\n\n## Introduction\n\nPrediction markets are the current breakout sector in crypto. In February 2026, the sector processed [$23.2 billion](https://dune.com/datadashboards/prediction-markets) in trading volume, up 1,218% YoY from [$1.8 billion](https://dune.com/datadashboards/prediction-markets) in February 2025. Polymarket and Kalshi led that expansion, ranking among the top two platforms by monthly volume, open interest, transaction count, and unique users for almost every week of 2025.\n\n\n\nFrom February 2025 to February 2026, Polymarket's monthly trading volume grew 427% from [$1.5 billion](https://dune.com/queries/6689536/10534249) to [$7.9 billion](https://dune.com/queries/6689536/10534249). Monthly transactions grew 2,206% from [3.5 million](https://dune.com/queries/6689539/10534256) to [80.7 million](https://dune.com/queries/6689539/10534256), and active users grew 58% from [426,000](https://dune.com/queries/6689540/10534259) to [671,400](https://dune.com/queries/6689540/10534259) over the same period. \n\nOpen interest (OI) measures the capital at risk across unresolved markets, offering a cleaner view of platform activity than volume because it cannot be inflated by wash-traded markets. From March 1, 2025, to February 28, 2026, Polymarket's OI grew 262% from [$107.5 million](https://dune.com/queries/5749464/9330387) to [$389.0 million](https://dune.com/queries/5749464/9330387). \n\nThat dominance drew investment capital at scale in 2025 as Polymarket raised three rounds of funding:\n\n* On [June 25, 2025](https://messari.io/project/polymarket/fundraising/funding), it raised a $185 million Series C led by Multicoin Capital.\n* On [August 26, 2025](https://messari.io/project/polymarket/fundraising/funding), it completed a $150 million strategic round led by Coinbase Ventures. \n* On [October 7, 2025](https://messari.io/project/polymarket/fundraising/funding), Intercontinental Exchange, the parent company of the New York Stock Exchange, agreed to invest up to $2 billion in a commercial and regulatory partnership that valued Polymarket at roughly $9 billion.\n\n**On [March 7, 2026](https://www.wsj.com/finance/kalshi-and-polymarket-are-each-eyeing-roughly-20-billion-valuations-d7b9c5d8), Polymarket was reportedly sounding out investors for funding rounds at a $20 billion fully diluted valuation (FDV). This report builds a ground-up valuation of Polymarket to test whether that FDV is justified.** \n\nVenture and institutional capital funded the platform's growth, then attention turned to whether a public token would arrive. On [October 24, 2025](https://www.coindesk.com/markets/2025/10/24/polymarket-will-launch-token-and-airdrop-after-u-s-relaunch-cmo-says), Polymarket CMO Matthew Modabber confirmed plans for a POLY token and a future airdrop. In [February 2026](https://messari.io/copilot/share/polymarket-airdrop-rumors-a36ebae6-fc4d-4db0-b967-a4302d6cbb44), expectations shifted toward a launch before the end of August 2026, after a [Polymarket team member](https://x.com/mustafap0ly) liked an X post stating that the platform would conduct an airdrop within that timeframe. The timing remains unconfirmed, but a 2026 launch appears increasingly likely. Whether that growth translates to durable value capture for POLY holders is the central question for investors. \n\nThe platform has proven product-market fit, and the fundraising validates institutional conviction. Polymarket generated minimal revenue for most of its existence, as taker fees launched on January 6, 2026, limited to select crypto and sports markets, and the majority of markets remained fee-free. On [March 23, 2026](https://docs.polymarket.com/trading/fees), Polymarket announced plans to extend taker fees to all markets except geopolitical, [effective March 30](https://docs.polymarket.com/trading/fees), with varying maximum effective fee rates across categories. **The path from product-market fit to token value accrual will depend on how well Polymarket retains volume share after its fee expansion.**\n\nThis report focuses on [Polymarket (global)](https://polymarket.com/) and refers to it as \"Polymarket\" throughout. This report does not cover [Polymarket U.S.](https://www.polymarketexchange.com/) or its valuation, as it is a [separate legal entity](https://polymarket.com/tos#:~:text=Polymarket%20operates%20globally,Privacy%20Policy.) from Polymarket (global). \n\n## Understanding Polymarket\n\n[Polymarket](https://messari.io/project/polymarket) is an onchain prediction market where users trade tokens tied to the outcome of future events. Markets cover questions such as _“[Will Marco Rubio win the 2028 U.S. Presidential Election?](https://polymarket.com/event/presidential-election-winner-2028),”_ with each market having binary Yes or No tokens tied to the outcome. Yes and No tokens trade between $0.00 and $1.00 in [USDC.e](https://messari.io/project/usd-coin-ethereum-bridged) (bridged [USDC](https://messari.io/project/circle-usdc)), and each pair of these tokens is fully collateralized by $1.00 of USDC.e. The collateral is locked in a [Conditional Token Framework (CTF)](https://docs.polymarket.com/trading/ctf/overview) contract, an open standard built by [Gnosis](https://github.com/gnosis/conditional-tokens-contracts/).\n\nNew tokens are minted through a process called [splitting](https://docs.polymarket.com/concepts/positions-tokens#split): when a user splits $1 of USDC.e collateral, the CTF mints two [ERC1155](https://messari.io/copilot/share/erc1155-token-standard-explained-a910557b-9763-44ee-b010-b19786941192) tokens, 1 Yes token and 1 No token, representing each side of the binary market. For example, splitting $100 USDC.e produces 100 Yes tokens + 100 No tokens.\n\nThe reverse process is called [merging](https://docs.polymarket.com/concepts/positions-tokens#merge): when a user converts equal amounts of Yes and No tokens back into USDC.e. For example, merging 100 Yes tokens + 100 No tokens converts them into $100 USDC.e.\n\nIf the market outcome is Yes, each Yes token pays $1.00, and each No token settles at $0. If the outcome is No, the payouts reverse. A $0.65 token price implies a 65% market-implied probability that the event occurs. \n\nPolymarket does not restrict high-performing users from trading because all bets are peer-to-peer, meaning Polymarket never takes the other side of a trade and carries no house risk. Traditional sportsbooks like [DraftKings](https://ca.finance.yahoo.com/quote/DKNG/) and [FanDuel](https://ca.finance.yahoo.com/quote/FLUT/) [ban profitable bettors](https://fairoddsterminal.com/why-modern-sports-betting-different) because the platforms trade directly against their customers and absorb losses when those customers win.\n\nPolymarket is onchain and does not require Know Your Customer (KYC) identity verification. [Polymarket U.S.](https://polymarket.com/usa), which is not covered in this report, operates as a Designated Contract Market (DCM) regulated by the Commodity Futures Trading Commission (CFTC) and requires KYC. \n\n### Technical Architecture\n\n**Events and Markets**\n\nPolymarket organizes prediction markets into two layers: [events](https://docs.polymarket.com/concepts/markets-events#events) and [markets](https://docs.polymarket.com/concepts/markets-events#markets). An event is a container that groups one or more related markets. A market is the core unit of trading on Polymarket. Each market poses a single binary question with a Yes or No outcome.\n\n\n\nSingle-market events contain only one market. For example, _\"Will Bitcoin reach $100,000 by December 2024?\"_ is both the event and the market. Multi-market events occur when an event has two or more mutually exclusive outcomes. For example, the event _“Who will win the 2024 Presidential Election?”_ ran as one event with multiple separate Yes/No markets:\n\n* _Market: Donald Trump? (Yes/No)_\n* _Market: Joe Biden? (Yes/No)_\n* _Market: Kamala Harris? (Yes/No)_\n* _Market: Other? (Yes/No)_\n\n**Trade Execution**\n\nTraders buy and sell these tokens through a hybrid onchain [central limit order book (CLOB)](https://docs.polymarket.com/concepts/prices-orderbook#:~:text=Central%20Limit%20Order%20Book%20(CLOB)). Polymarket stores orders, and its [operator matches orders offchain](https://docs.polymarket.com/concepts/prices-orderbook#how-trades-work).\n\n\n\n\n\n_Source: [Polymarket Documentation (prices & orderbook)](https://docs.polymarket.com/concepts/prices-orderbook)_\n\nOnce Polymarket matches orders, the trades settle [onchain](https://docs.polymarket.com/concepts/prices-orderbook#how-trades-work) on [Polygon](https://messari.io/project/polygon-ecosystem-token). Two order types are available: market orders execute immediately at the best available price, and limit orders sit in the order book until a counterparty matches them at the specified price. Traders can cancel unfilled limit orders at any time.\n\n**Resolution**\n\nWhen a market's end date passes, it enters the resolution phase. Polymarket uses [UMA's Optimistic Oracle](https://docs.polymarket.com/concepts/resolution#:~:text=UMA%20Optimistic%20Oracle), a permissionless resolution system, to resolve markets. Each market has pre-defined resolution rules specifying the outcome source of truth, market end date, and guidance for edge cases.\n\n\n\n_Source: [Polymarket Documentation (resolution)](https://docs.polymarket.com/concepts/resolution)_\n\nThe resolution process starts with a proposal. Any user can propose an outcome by selecting the winning side and posting a bond, [typically $750 USDC.e](https://docs.polymarket.com/concepts/resolution#:~:text=Posting%20a%20bond%20(typically%20%24750%20USDC.e)). If no one disputes the proposal within [two hours](https://docs.polymarket.com/concepts/resolution#:~:text=2%2Dhour%20challenge%20period), the market resolves and the proposer recovers their bond plus a reward. A dispute requires the challenger to post a matching $750 counter-bond, which opens a second proposal round. If that second proposal is also disputed, the question escalates to UMA's Data Verification Mechanism (DVM). DVM resolution is a [24-48 hour debate period](https://docs.polymarket.com/concepts/resolution#:~:text=During%20the%2024%2D48%20hour%20debate%20period) during which participants submit evidence on UMA's Discord advocating for their outcome, followed by a 48-hour vote by UMA token holders. \n\nThe [DVM vote](https://docs.polymarket.com/concepts/resolution#:~:text=After%20the%20debate%20period%2C%20UMA%20token%20holders%20vote%20on%20the%20correct%20outcome) produces one of four outcomes:\n\n* **Proposer wins:** Original proposal accepted. Proposer recovers their bond plus half of the disputer's bond.\n* **Disputer wins:** Proposal rejected, which requires a new proposal. Disputer recovers their bond plus half of the proposer's bond.\n* **Too Early:** Event has not yet concluded. Disputer recovers their bond plus half of the proposer's bond.\n* **Unknown / 50-50:** Neither outcome applies. The market resolves at 50/50, which means each token redeems for $0.50, and the disputer recovers their bond plus half of the proposer's bond.\n\nPolymarket's hybrid CLOB makes binary prediction markets intuitive for non-crypto-native users, and onchain settlement on Polygon provides transparent, verifiable execution once a trade is matched. The design holds up well on the surface, but the architecture carries two structural risks. \n\nFirst, offchain order matching gives Polymarket direct control over a centralized layer in the trade flow, exposing users to censorship or downtime risks. Second, UMA's DVM introduces resolution risk when voting power concentrates among a small number of large UMA token holders. Smaller token holders face slashing penalties for voting against the majority, creating a structural incentive to follow whale votes rather than seek truthful outcomes.\n\n\n\n_Source: [The Defiant](https://thedefiant.io/news/defi/polymarket-s-usd7m-ukraine-mineral-deal-debacle-traced-to-oracle-whale)_\n\nOn [March 24, 2025](https://www.theblock.co/post/348171/polymarket-says-governance-attack-by-uma-whale-to-hijack-a-bets-resolution-is-unprecedented), this vulnerability surfaced on a market asking, \"Ukraine agrees to Trump mineral deal before April?\" A user placed a large bet on Yes despite no official agreement existing, and proposed a Yes resolution. The proposal was disputed, and during the vote, a validator cast [5 million UMA tokens across three accounts](https://thedefiant.io/news/defi/polymarket-s-usd7m-ukraine-mineral-deal-debacle-traced-to-oracle-whale), representing 25% of total votes, in favor of Yes, steering the vote toward an incorrect outcome. The market resolved in favor of Yes. Polymarket called it an \"unprecedented\" governance attack and confirmed it could not issue refunds. The incident was isolated, and Polymarket has implemented changes to the resolution system since the attack, but the structural vulnerability in UMA's voting mechanics remains open.\n\n### Revenue Model\n\nPolymarket charges [no fees](https://docs.polymarket.com/polymarket-learn/trading/fees) on deposits or withdrawals and [covers](https://docs.polymarket.com/trading/gasless#what-is-covered) all Polygon gas fees for outcome token trades and approvals. Until January 2026, the platform generated no direct trading revenue.\n\nOn [January 6, 2026](https://www.gncrypto.news/news/polymarket-introduces-fees-15-minute-markets/), Polymarket introduced taker fees on 15-min crypto markets, its first direct monetization of trading activity. In February 2026, taker fees expanded to 5-min crypto markets and select sports markets, specifically NCAAB and Serie A. On [March 23, 2026](https://docs.polymarket.com/trading/fees#markets-with-fees), Polymarket announced **taker fees would extend to all markets except geopolitical**, effective [March 30](https://docs.polymarket.com/trading/fees#markets-with-fees), with varying maximum effective fee rates across categories. Polymarket charges **no maker fees on any market.**\n\n\n\n_Source: [Polymarket Documentation (fees)](https://docs.polymarket.com/trading/fees)_\n\n[Taker fees](https://docs.polymarket.com/trading/fees#fee-structure) vary by price per share, peak at 50% probability, and decrease symmetrically toward the extremes. Crypto markets charge the highest peak effective fee rate (for 100 shares), [at 1.80%](https://docs.polymarket.com/trading/fees#fee-structure). A trader buying 100 shares at a 50% probability pays a $0.90 taker fee on a $50 trade. \n\nMentions markets charge the next highest [peak rate at 1.56%,](https://docs.polymarket.com/trading/fees#fee-structure) with a $0.78 taker fee on the same $50 trade. Sports markets charge the lowest peak rate of any fee-charging market, [at 0.75%](https://docs.polymarket.com/trading/fees#fee-structure), a $0.38 taker fee on a $50 trade.\n\nOn buy orders, Polymarket collects taker fees in outcome shares rather than USDC.e. A trader buying 100 contracts at $0.50 receives fewer shares: the $0.90 fee is deducted from the position, delivering 98.20 shares instead of 100. On sell orders, the fee is deducted directly from the USDC.e proceeds the trader receives.\n\nBy comparison, Kalshi charges taker fees on [most markets](https://kalshi.com/fee-schedule), peaking at 50% probability, but charges an [effective peak fee rate of 3.5%](https://kalshi.com/docs/kalshi-fee-schedule.pdf), more than double Polymarket's crypto peak. On the same $50 trade, a Kalshi user pays $1.75.\n\nTo compensate liquidity providers on fee-bearing markets, Polymarket operates a [**maker rebate**](https://docs.polymarket.com/market-makers/maker-rebates) program. Effective March 30, rebates are [50% for finance](https://docs.polymarket.com/trading/fees#markets-with-fees) markets, [20% for crypto](https://docs.polymarket.com/trading/fees#markets-with-fees) markets, and [25% for all other](https://docs.polymarket.com/trading/fees#markets-with-fees) fee-charging markets. Rebates are paid daily in USDC.e based on a maker's proportional share of taken liquidity.\n\n\n\nFrom January 6 to March 25, Polymarket generated [$1.8 million in taker fees](https://dune.com/queries/6538205/10339674), with fees limited to crypto and select sports markets. Effective March 30, taker fees apply to nearly all Polymarket markets. Kalshi has charged taker fees throughout its existence and, as of [March 25](https://dune.com/datadashboards/kalshi-overviewhttps://dune.com/datadashboards/kalshi-overview), generated [$56.3 billion in cumulative volume](https://dune.com/queries/5910828/9546583), suggesting prediction market users tolerate fees when the underlying product is compelling. \n\n**The question is whether Polymarket demand proves inelastic or compresses as users encounter fees for the first time.**\n\n### POLY Token Utility\n\nPolymarket has not released an official utility framework or value capture mechanism for the POLY token. On [October 24, 2025](https://www.coindesk.com/markets/2025/10/24/polymarket-will-launch-token-and-airdrop-after-u-s-relaunch-cmo-says), Polymarket CMO Matthew Modabber confirmed plans for a POLY token and a future airdrop. During this announcement, [he stated](https://www.coindesk.com/markets/2025/10/24/polymarket-will-launch-token-and-airdrop-after-u-s-relaunch-cmo-says), \"We want POLY to be a token with true utility and longevity, and to be around forever.\" \n\nThree areas of Polymarket's architecture point to where that POLY utility could materialize, the first is liquidity provider incentives. **We believe that over time, market accuracy will become the core product of prediction markets.** Accuracy requires liquidity, and liquidity requires incentives. POLY rewards on top of existing USDC.e maker rebates would give market makers a direct reason to provide deeper liquidity, tightening spreads, and improving the probability accuracy that institutional partners like the NYSE already demand.\n\nThe second is resolution staking. POLY could replace UMA tokens as the staking collateral for proposing and disputing market resolutions, with correct voters earning tokens and incorrect voters losing them. Beyond potential improvements to the existing vulnerabilities in their UMA optimistic oracle architecture, this mechanism would tie token demand directly to the platform's core function.\n\nThe third is fee rebates for POLY stakers. A staking-based taker fee discount would create a direct incentive for high-volume traders to accumulate and hold POLY, tying token demand to platform usage in the same way trading fee discounts have worked on centralized exchanges.\n\nNone of these mechanisms have been confirmed. Each draws on established DeFi precedent and fits Polymarket's existing architecture. Investors should treat them as informed speculation until Polymarket makes an official announcement.\n\n## State of Polymarket\n\nFrom January 2025 through August 2025, Polymarket ranked first among prediction markets by trading volume, with [72% share ($12.0 billion)](https://dune.com/queries/6689536/10534249) in cumulative notional volume. \n\nCompetition intensified over the last six months as Polymarket's position shifted from dominant to contested. From September 2025 through February 2026, Kalshi led prediction markets with a [40% share ($39.6 billion)](https://dune.com/queries/6689536/10534249), followed by Polymarket at [31% ($32.1 billion)](https://dune.com/queries/6689536/10534249) and Opinion at [23% ($22.9 billion)](https://dune.com/queries/6689536/10534249).\n\n\n\nDespite the share loss, the underlying business continued to grow across all key metrics. From September 2025 to February 2026, Polymarket's monthly trading volume grew 383%, from [$1.6 billion to $7.9 billion](https://dune.com/datadashboards/polymarket-overview). Monthly transactions grew 1,385%, from [5.4 million to 80.7 million](https://dune.com/datadashboards/polymarket-overview). Monthly active users grew 172%, from [246,600 to 671,400](https://dune.com/datadashboards/polymarket-overview). From September 30, 2025, to February 28, 2026, OI grew 141% from [$161.3 million to $389.0 million](https://dune.com/datadashboards/polymarket-overview). \n\nTwo factors drove this growth. The first is expanding mindshare. Prediction markets, specifically Polymarket and Kalshi, entered mainstream awareness in 2025 through significant marketing campaigns and media partnerships. In Q4 2025, Polymarket secured partnerships with the [NHL](https://www.nhl.com/news/nhl-announces-landmark-multiyear-partnerships-with-kalshi-polymarket), [UFC](https://www.cnbc.com/2025/11/13/tko-polymarket-strike-multiyear-deal-to-integrate-prediction-markets-into-ufc-events.html), [Golden Globe Awards](https://variety.com/2026/film/news/polymarket-golden-globes-prediction-market-partner-1236627204/), and others, each of which embedded Polymarket odds directly into live broadcasts and partner platforms. For many non-crypto-native users, this was their first exposure to prediction markets, and the media distribution converted passive audiences into active participants on the platform.\n\nThe second is airdrop farming. Polymarket was already growing organically before the POLY announcement, but the token announcement was a clear accelerant, and separating organic demand from farming activity in current volume figures is difficult.\n\nBefore the POLY airdrop announcement on October 24, 2025, the single-largest-volume month in Polymarket's history was October 2024, with [$4.3 billion in volume](https://dune.com/queries/6689536/10534249), driven by the U.S. Presidential Election. After Modabber's airdrop announcement, November 2025 generated [$4.4 billion in volume](https://dune.com/queries/6689536/10534249), and every month since has surpassed October 2024's record by a significant margin. While Polymarket was already growing organically, the POLY airdrop announcement likely contributed additional demand from farming activity on top of existing organic growth.\n\nFrom September 2025 to February 2026, Kalshi’s monthly trading volume grew 259%, from [$2.9 billion to $10.4 billion](https://dune.com/datadashboards/polymarket-overview). This growth occurred without an airdrop announcement, suggesting genuine growing interest in prediction markets rather than volume driven by farming activity on Polymarket. While Polymarket's mainstream penetration suggests a strong volume floor, post-airdrop protocols typically [retain 10-20% of pre-airdrop volume](https://paragraph.com/@sixdegreelab-3/chapter-1-retention-a-review-by-sixdegree-of-airdrop-and-liquidity-mining#:~:text=Selected%20airdrops%20including%201inch%2C%20Uniswap%2C%20Optimism%2C%20Arbitrum%20and%20ParaSwap%20have%20a%20retention%20rate%20under%2020%25%20after%20four%20months%20and%20under%2015%25%20after%2012%20months), and investors should treat current volume figures with some caution until post-TGE retention data is available.\n\n\n\nPolymarket's volume is distributed across three primary categories: sports, politics, and crypto. In February 2026, sports led with a [37% share ($3.0 billion)](https://dune.com/queries/5910984/9546787), followed by [crypto at 30% ($2.4 billion)](https://dune.com/queries/5910984/9546787) and [politics at 28% ($2.2 billion)](https://dune.com/queries/5910984/9546787). Other categories, led by culture and economy markets, accounted for the remaining [5% share ($342.8 million)](https://dune.com/queries/5910984/9546787). \n\nAs of February 28, Polymarket had $389.0 million in OI, with the same top three categories in a different order. Politics led with a [60% share ($232.9 million)](https://dune.com/queries/5910984/9546787), followed by [sports at 17% ($67.0 million)](https://dune.com/queries/5910984/9546787) and [crypto 16% ($64.1 million)](https://dune.com/queries/5910984/9546787). Other categories accounted for the remaining [7% share ($25.0 million)](https://dune.com/queries/5910984/9546787).\n\nPolymarket has three independent categories driving volume, which is a key strength, but each operates on different catalysts. Sports volume follows fixed seasonal schedules and marquee events, with the NFL season providing the highest-volume window each year. Politics volume is cyclical, peaking around U.S. elections, with the 2026 midterms and 2028 presidential cycle representing the next natural volume catalysts. Crypto volume is driven by 5-min and 15-min up/down markets launched in October 2025, which generate high turnover through short resolution cycles. Each category's growth trajectory differs, so we modeled them separately in the valuation section.\n\nWith Polymarket's market position established, we turn to valuation. The core question is whether the [$20 billion FDV](https://www.wsj.com/finance/kalshi-and-polymarket-are-each-eyeing-roughly-20-billion-valuations-d7b9c5d8) Polymarket was reported to be seeking from investors on March 7 reflects reasonable expectations for future fee generation, or whether the market is mispricing the opportunity.\n\n## Valuing Polymarket (POLY)\n\nPolymarket is valued on a multiple of projected 2028 fees. Polymarket operates as a pure-play prediction market with no L1 monetary premium or diversified revenue streams, making fee generation the appropriate valuation basis. Taker fees launched on January 6, 2026, and as of March 30, are effective across all markets except geopolitical. Revenue before March 30 does not represent steady-state monetization, as taker fees only recently expanded beyond crypto and sports markets. Projecting to 2028 provides sufficient runway for the fee rollout to mature across all fee-charging categories.\n\nThis valuation is based solely on Polymarket’s volume and fee projections. Polymarket U.S. operates as a separate legal entity and is excluded from this analysis.\n\nPrediction markets remain a relatively nascent primitive, and each major category operates on structurally different catalysts with distinct growth trajectories. Projecting against a single aggregate TAM would obscure these dynamics. We model sports, politics, crypto, and other categories independently and map out the bear, base, and bull cases using six assumptions that cover four category-specific volume projections, take rates, and multiples. \n\n_Our full valuation model can be viewed [here](https://docs.google.com/spreadsheets/d/1JpRHkS--eHIii_P-PhsM1nrOJtfi56Qmg17qO6J9Mqk/edit?usp=sharing)._\n\n### Polymarket Category Volume Assumptions\n\n#### Sports volume\n\nTo calculate the growth rate, we compared Polymarket sports volumes during _September 2024 to February 2025 ([$6.2 billIion](https://dune.com/queries/5910984/9546787)) with those from September 2025 to February 2026 ([$10.5 billion](https://dune.com/queries/5910984/9546787))_. This window is annually the highest-volume period in U.S. sports betting, driven by the NFL season. Measuring the same period in subsequent years provided a like-for-like basis for isolating the true volume trajectory.\n\nThis comparison yielded a 68% YoY growth rate. We expect the base growth rate to be below 68% due to potential Polymarket U.S. volume cannibalization. To account for these factors, **we applied growth rates of 30%, 50%, and 100% in our bear, base, and bull cases, respectively.**\n\nIn 2025, Polymarket generated [$10.6 billion in sports volume](https://dune.com/queries/5910984/9546787), and we applied the above growth rates to this figure to arrive at our 2028 projections.\n\nWe benchmarked these projections against the 2028 global sportsbook handle. In 2025, the U.S. sportsbook handle reached [$165.0 billion](https://www.sportsbookreview.com/news/us-betting-revenue-tracker/). Assuming global legal sportsbook handle equals 2x the U.S. handle, a conservative estimate, the 2025 global handle stood at approximately $330.0 billion. The global legal sportsbook handle grew at a [10% CAGR from 2022 to 2025](https://www.igamingdirect.com/reports/2025/06/19/2025-global-sports-betting-market-growth-report/#:~:text=CAGR%20(2021%E2%80%932025)%3A%2010.3%25). Applying that rate forward, the 2028 global sportsbook handle will reach $442.8 billion.\n\n* **Bear:** 30% YoY growth brings Polymarket sports volume to $23.3 billion by 2028, 5% of the projected 2028 global sportsbook handle. Competition intensifies from incumbent sportsbooks, Kalshi, and other onchain entrants like Opinion, Novig, and Hyperliquid, while Polymarket U.S. cannibalizes domestic sports volume from the global platform.\n* **Base:** 50% YoY growth brings Polymarket sports volume to $35.7 billion by 2028, 8% of the projected 2028 handle. New users continue onboarding, and average volume per wallet increases. As of January 13, 2026, [59% of Polymarket wallets](https://messari.io/report/polymarkets-best-growth-path#:~:text=59%25%20(1.1%20million,moving%20the%20price.) had bet less than $1,000 in all-time volume. In 2024, DraftKings averaged [$13,000 annual volume per user](https://messari.io/report/polymarkets-best-growth-path#:~:text=user%2C%20or%20about-,%2413%2C000%20annualized,-.%20That%20single%2Dyear), meaning most Polymarket wallets have significant room to grow before reaching traditional sportsbook levels.\n* **Bull:** 100% YoY growth brings Polymarket sports volume to $84.7 billion by 2028, 19% of the projected 2028 handle. Traditional sportsbook users migrate significantly to Polymarket as peer-to-peer pricing advantages in prediction markets become widely recognized and distribution improves.\n\n\n\n#### Politics volume\n\nPolitics volume is heavily correlated to the U.S. Presidential election cycle, with volume concentrated in the months immediately preceding and during the election. This surge was evident from [September through November 2024](https://dune.com/queries/5910984/9546787). To exclude this influence and isolate the underlying growth trajectory, we compared volume during _January to June 2025 ([$3.6 billion](https://dune.com/queries/5910984/9546787)) with that from July to December 2025 ([$5.2 billion](https://dune.com/queries/5910984/9546787))_, periods unaffected by election-driven demand.\n\nThis comparison resulted in a **46% increase, which we used as our base growth rate**. The **bear and bull cases apply 0.5x and 2x multipliers, resulting in 23% and 92%, respectively.**\n\nOn top of the base growth rate, we applied election-cycle multipliers to capture the structural volume boost from the U.S. political calendar: a 20% multiplier in 2026 to account for the midterm elections, and a 40% multiplier in 2028 for the U.S. presidential election. We calculated the presidential election multiplier by comparing 2024 annualized politics volume ([$12.0 billion](https://dune.com/queries/5910984/9546787)) against the 2025 volume ([$8.7 billion](https://dune.com/queries/5910984/9546787)). This resulted in a 40% difference, which reflects the volume uplift from a presidential election year. We applied half that rate, 20%, for midterm elections.\n\nIn 2025, Polymarket generated [$8.7 billion in political volume](https://dune.com/queries/5910984/9546787), and we applied the above growth rates (plus election multipliers) to this figure to arrive at our 2028 projections.\n\n* **Bear:** 23% YoY growth (plus election multipliers) brings Polymarket politics volume to $18.1 billion by 2028. Competition from Kalshi, Robinhood, and traditional sportsbooks entering political markets erodes Polymarket's first-mover advantage as the category matures.\n* **Base:** 46% YoY growth (plus election multipliers) brings Polymarket politics volume to $32.4 billion by 2028. The base growth rate holds as traditional finance firms increasingly adopt political markets as macro hedging tools for regulatory and trade policy outcomes.\n* **Bull:** 92% YoY growth (plus election multipliers) brings Polymarket politics volume to $80.2 billion by 2028. Non-U.S. interest in U.S. political outcomes drives significant international demand, and mainstream media adoption of political odds as a standard reference tool creates a self-reinforcing awareness cycle. Polymarket Global experiences minimal cannibalization from Polymarket U.S.\n\n\n\n#### Crypto volume\n\nOn [October 21, 2025](https://www.binance.com/en/square/post/31303183204065), Polymarket launched [15-min up/down markets](https://polymarket.com/crypto) for [BTC](https://polymarket.com/crypto/bitcoin), [ETH](https://polymarket.com/crypto/ethereum), [SOL](https://polymarket.com/crypto/solana), and [XRP](https://polymarket.com/crypto/xrp), followed shortly by [5-min markets](https://polymarket.com/crypto). Crypto volume spiked after these launches, creating a sharp jump in activity that is unlikely to repeat.\n\nComparing volume from before and after this launch would overstate long-term growth, since it would treat this one-time jump as sustainable. To avoid that, we compared two equal 10-week periods after the spike: _October 27, 2025, to January 4, 2026 ([$2.8 billion](https://dune.com/queries/5910984/9546779)),_ and _January 5 to March 8, 2026 ([$5.5 billion](https://dune.com/queries/5910984/9546779))._ This isolated volume growth after the new baseline was established.\n\nThis comparison resulted in a **92% increase, which we used as our base growth rate.** **The bear and bull cases apply 0.5x and 2x multipliers, resulting in 46% and 184%, respectively.**\n\nIn 2025, Polymarket generated [$5.4 billion in crypto volume](https://dune.com/queries/5910984/9546787), and we applied the above growth rates to this figure to arrive at our 2028 projections.\n\n* **Bear:** 46% YoY growth brings Polymarket crypto volume to $16.9 billion by 2028. After POLY TGE, volume contracts sharply as airdrop farming washout occurs and 5-min and 15-min market novelty fades.\n* **Base:** 92% YoY growth brings Polymarket crypto volume to $38.3 billion by 2028. Fast-resolving markets prove durable after POLY TGE as institutional arbitrageurs enter on deeper liquidity, and [pre-market crypto events](https://polymarket.com/crypto/pre-market) (i.e., pre-TGE, or Pre-IPO projections) find product-market fit.\n* **Bull:** 184% YoY growth brings Polymarket crypto volume to $123.7 billion by 2028. Fast-resolving markets establish themselves as the dominant crypto speculation vertical, and markets expand into new timeframes and assets. [Pre-market crypto events](https://polymarket.com/crypto/pre-market) find strong product-market fit (i.e., as a hedging tool for private investors).\n\n\n\n#### Other volume\n\nThe ‘other’ category covers all markets outside Polymarket's core three verticals, with culture and economy leading the segment in 2025 volume. To set a baseline, we compared average weekly volume over the last eight weeks of 2024 ([$38.7 million](https://dune.com/queries/5910984/9546787)) against the 2025 full-year weekly average ([$56.2 million](https://dune.com/queries/5910984/9546787)).\n\nWe chose that window to exclude the November 2024 U.S. presidential election spike. Before the 2024 U.S. presidential election, Polymarket had almost no mainstream audience, so ‘other’ markets generated low volume. The election drew thousands of new users to the platform, and after it ended, those users stayed and began trading culture, economy, and other markets. Using full-year 2024 as a baseline would average in nine months of negligible volume, so we anchored to the last eight weeks of 2024, the first period where ‘other’ markets had a real user base behind them.\n\nThis comparison resulted in a **45% increase, which we used as our base growth rate. The bear and bull cases apply 0.5x and 2x multipliers, resulting in 23% and 90%, respectively.**\n\nIn 2025, Polymarket generated [$2.9 billion in ‘other’ category volume](https://dune.com/queries/5910984/9546787), and we applied the above growth rates to this base to arrive at our 2028 projections.\n\n* **Bear:** 23% YoY growth brings ‘other’ category volume to $5.4 billion by 2028. Experimental categories fail to find sustained product-market fit, liquidity remains too thin for institutional use cases, and users concentrate activity in the core Sports, Politics, and Crypto verticals.\n* **Base:** 45% YoY growth brings ‘other’ category volume to $9.0 billion by 2028. A few categories break out, such as economic indicators, culture markets, or weather hedging.\n* **Bull:** 90% YoY growth brings ‘other’ category volume to $20.3 billion by 2028. Multiple categories achieve product-market fit simultaneously. For example, weather derivatives attract institutional hedging demand, economic indicator markets establish themselves as macro trading tools, and culture markets expand as liquidity deepens.\n\n\n\n### Monetization Assumptions \n\n#### Take Rate \n\n**We assume Polymarket's take rate equals 50 bps, 70 bps, and 90 bps in our bear, base, and bull cases, respectively.** For our lower bound, we assume that Polymarket’s take rate starts to converge towards Robinhood's Q4 2025 crypto take rate of [27 bps](https://investors.robinhood.com/news-releases/news-release-details/robinhood-reports-fourth-quarter-and-full-year-2025-results) ([$221 million in fees from $82 billion in volume](https://investors.robinhood.com/news-releases/news-release-details/robinhood-reports-fourth-quarter-and-full-year-2025-results)), but still remains elevated in 2028. For our upper bound, we assumed that Polymarket’s take rate will remain below Kalshi’s 2025 take rate of [115 bps](https://finance.yahoo.com/news/kalshi-fee-revenue-2025-263-145801350.html) ([$263.5 million in fees from $22.9 billion in volume](https://finance.yahoo.com/news/kalshi-fee-revenue-2025-263-145801350.html)).\n\nPolymarket launched taker fees on select crypto markets on January 6, 2026, and expanded to nearly all markets effective March 30, 2026. We expect the take rate to increase as fee-bearing volume scales across categories through 2028.\n\n* **Bear:** Take rate equals 50 bps. Competition from Kalshi and emerging platforms limits pricing power, and peak effective fee rates compress as the prediction market sector matures.\n* **Base:** Take rate equals 70 bps. Polymarket peak effective fee rates established on March 30 remain intact.\n* **Bull:** Take rate equals 90 bps. Polymarket increases peak effective fee rates for all high-volume markets. At 90 bps, the Polymarket’s projected bull take rate remains below Kalshi's 2025 take rate, reflecting competitive compression as prediction market pricing normalizes over the next three years.\n\n\n\n#### Multiple\n\n\n\nWe assume Polymarket trades at 20x, 30x, and 40x fees in our bear, base, and bull cases, respectively. These multiples are applied to the 2028 projected fees. On [March 19, 2026](https://www.bloomberg.com/news/articles/2026-03-19/kalshi-gets-1-billion-in-new-funding-at-22-billion-valuation), Kalshi raised $1 billion at a [$22 billion valuation](https://www.bloomberg.com/news/articles/2026-03-19/kalshi-gets-1-billion-in-new-funding-at-22-billion-valuation). With [$263.5 million in 2025 fees](https://finance.yahoo.com/news/kalshi-fee-revenue-2025-263-145801350.html), the $22 billion FDV equals an 83.5x fees multiple. We used that multiple as a ceiling for the prediction markets sector. As fee growth is realized through 2028, Kalshi's implied multiple will compress naturally. Our 2028 bull case multiple of 40x is therefore more conservative than Kalshi's current 83.5x multiple.\n\n\n\n* **Bear:** The market assigns a 20x multiple on weak growth visibility and unconfirmed POLY value accrual. Take rate stalls below expectations, post-TGE volume contraction weighs on projections, and POLY trades at a steep discount to peers with more defined token distribution mechanisms.\n* **Base:** The market assigns a 30x multiple on steady peak effective fee rates and volume growth projections. The market prices Polymarket as a credible but not leading protocol with a maturing fee structure.\n* **Bull:** The market assigns a 40x multiple on increasing peak effective fee rates, confirmed POLY utility, and Polymarket establishing itself as the dominant prediction market protocol. At 40x, POLY trades below Kalshi's implied 83x private round multiple, reflecting the typical compression between private and liquid token valuations and Polymarket's less mature fee structure.\n\n### Polymarket Valuation Results\n\nUnder our assumptions, Polymarket's base-case FDV is $24.2 billion by 2028, with a range from $6.4 billion (bear case) to $111.2 billion (bull case).\n\n\n\n* **Bear:** Total volume across all categories reaches $63.6 billion by 2028. A 50 bps take rate generates $318.0 million in annual fees. **At a 20x multiple, the implied FDV is $6.4 billion.**\n* **Base:** Total volume across all categories reaches $115.4 billion by 2028. A 70 bps take rate generates $807.9 million in annual fees. **At a 30x multiple, the implied FDV is $24.2 billion.**\n* **Bull:** Total volume across all categories reaches $309.0 billion by 2028. A 90 bps take rate generates $2.8 billion in annual fees. **At a 40x multiple, the implied FDV is $111.2 billion.**\n\n#### Interpretation\n\n**Under our base case, Polymarket reaches a $24.2 billion FDV by 2028**, just 21% above the $20 billion valuation Polymarket has been rumoured to seek as of [March 7, 2026](https://www.wsj.com/finance/kalshi-and-polymarket-are-each-eyeing-roughly-20-billion-valuations-d7b9c5d8). At $20 billion, investors would be paying just below base case execution with minimal upside remaining. The bear case at $6.4 billion represents substantial downside from current levels, and the risk is real: post-TGE volume retention and the blended take rate at scale remain unproven.\n\nTake rate and multiple are the primary valuation levers across bear, base, and bull cases. Multiple is market-assigned and reflects investor sentiment toward the prediction market category, POLY token utility, and growth expectations. Polymarket does not control it, while Polymarket does control taker fees. With taker fees now applicable to nearly all markets, effective March 30, the fee rates themselves are set. The blended take rate, however, moves with volume, and if it compresses in high-fee markets, the blended take rate falls with it. **Polymarket's focus now is adaptability: maximize fees in markets where demand is inelastic, and adjust rates down in markets where volume proves sensitive to price.** Sustaining volume growth in all fee-charging markets will determine whether the blended take rate reaches base case expectations.\n\nThe bull case implies a $111.2 billion FDV, 5.6x the rumoured $20 billion valuation. Reaching it **requires $309 billion in total 2028 volume, a 90 bps blended take rate, and a 40x market multiple. Each variable is achievable in isolation. Achieving all three simultaneously is the challenge.**\n\n### Sensitivity Tables\n\nWithin each scenario, the valuation remains sensitive to fees generated and the ‘multiple’ factor that together determine how projected fee generation translates into an implied FDV. To illustrate this relationship, we conducted a sensitivity analysis across all three scenarios.\n\n\n\n**In the bear case, Polymarket’s valuation clusters within a $600.0 million to $17.2 billion range across revenues of $159.0 to 477.0 million, and multiples of 4x to 36x.** The biggest unknown in the bear case is the multiple. While our bear case is 20x for this scenario, there are strong arguments to be made for a much lower multiple. For example, [DraftKings (DKNG)](https://finance.yahoo.com/quote/DKNG/) and [FanDuel (FLUT)](https://finance.yahoo.com/quote/FLUT/) trade at low P/S multiples (1.8x and 1.2x, respectively) due to the high-cost nature of running a sportsbook. If Polymarket falls into the same trap of high customer acquisition and retention costs that have harmed sportsbooks’ bottom line, then it will likely trade at the lower range of these multiples.\n\n\n\n**In the base case, Polymarket’s implied FDV spans a broader range of $3.1 billion to $65.4 billion, reflecting balanced sensitivity to both fees ($307.9 million to $1.3 billion) and multiples (10x to 50x).** The valuation responds more linearly to changes in assumptions, as outcomes are driven less by existential adoption risk and more by how investors price fee durability and growth optionality. This range provides the most informative valuation band, consistent with prediction markets, and Polymarket alongside it, establishing themselves as new, scalable market infrastructure that is able to capture previously underserved demand.\n\n\n\n**In the bull case, Polymarket’s valuation ranges from $26.0 billion to $258.0 billion, driven primarily by sensitivity to multiples (20x to 60x) and secondarily by fee outcomes ($1.3 billion to $4.3 billion).** The biggest unknown in the bull case is if Polymarket will be in the early or late stages of its growth cycle. If strong growth can be expected post-2028, it can retain a multiple closer to Kalshi’s current fee multiple of 83.5x. However, if the reverse is true and Polymarket’s post-2028 growth appears to be slowing down, it would like trade at a multiple more consistent with traditional exchange infrastructure, such as [CME](https://finance.yahoo.com/quote/CME/) (16.7x) and [NDAQ](https://finance.yahoo.com/quote/NDAQ/) (9.2x).\n\nThe sensitivity analysis underscores that Polymarket’s implied FDV is not a single point estimate but a spectrum shaped by fee outcomes and investor expectations. Our base-case estimate of $24.2 billion sits at the center of the base-case sensitivity range, providing a defensible valuation anchor while acknowledging both downside risk under weaker multiples and upside potential if Polymarket is re-rated as an institutional trading venue. At the current rumored $20.0 billion FDV, investors are underwriting base case execution with modest upside. However, the investors who got in during any of the 2025 rounds have significant upside for both the base and bull cases. \n\n## Risks \n\nPolymarket’s valuation rests on prediction market demand, protocol monetization, and competitive positioning that are far from certain. Below, we outline the key risk factors for Polymarket.\n\n### Legislative/Regulatory Scrutiny\n\nIn recent months, prediction markets have come under increased [scrutiny](https://www.nytimes.com/2026/03/23/opinion/prediction-markets-gambling.html) as they have grown in popularity, particularly as an alternative venue for sports-related speculation. Because prediction markets do not operate under the same regulatory framework as traditional sportsbooks, critics have argued that they function as unregulated gambling platforms.\n\nOn [March 23](https://www.wsj.com/finance/regulation/lawmakers-to-introduce-bipartisan-bill-banning-sports-bets-on-prediction-markets-17d2e272?gaa_at=eafs&gaa_n=AWEtsqcGDsdkO86Wf_WAlTkB8DJACD2GGsyOYC_u33wc3bgNjSeD0ytUzYGkvP6YjFg%3D&gaa_ts=69c43278&gaa_sig=MYenoMqdfI1EYq_Bwa5_9DhvATQO0ODbYEuoynYVd-ZGGrgyymlcIJ4h0tYbkj8a4yIJlE8n0LWkGXccxr3n3g%3D%3D), a bipartisan bill was [introduced](https://www.wsj.com/finance/regulation/lawmakers-to-introduce-bipartisan-bill-banning-sports-bets-on-prediction-markets-17d2e272?gaa_at=eafs&gaa_n=AWEtsqcGDsdkO86Wf_WAlTkB8DJACD2GGsyOYC_u33wc3bgNjSeD0ytUzYGkvP6YjFg%3D&gaa_ts=69c43278&gaa_sig=MYenoMqdfI1EYq_Bwa5_9DhvATQO0ODbYEuoynYVd-ZGGrgyymlcIJ4h0tYbkj8a4yIJlE8n0LWkGXccxr3n3g%3D%3D) in the U.S. Senate seeking to prohibit prediction markets from offering contracts tied to sporting events. Should regulators impose further restrictions on the types of contracts that can be offered, or on prediction markets more broadly, Polymarket’s trading volumes and growth trajectory could be materially impacted.\n\n### Polymarket U.S. Cannibalization\n\nAs noted earlier, Polymarket (global) and Polymarket U.S. operate as separate legal entities. This report focuses solely on Polymarket (global). If the value generated by the U.S. entity does not accrue to the global entity, there is a risk of economic cannibalization.\n\nFor example, if future growth, particularly in high-volume verticals such as sports, occurs primarily within Polymarket U.S., then Polymarket (global) may experience slower growth or declining relative market share.\n\n### High Customer Acquisition Costs\n\nPrediction markets share structural similarities with sportsbooks, particularly in terms of user acquisition and retention dynamics. Historically, sportsbooks have incurred high customer acquisition costs through aggressive promotions and marketing campaigns.\n\nIf switching costs between prediction market platforms remain low, Polymarket may need to rely on similar incentives to attract and retain users. This could compress margins by offsetting fee revenue with higher marketing and promotional expenses.\n\n### Increased Competition\n\nThe prediction market sector is experiencing rapid growth, leading to increased competition. Kalshi has grown meaningfully to the point where the market could be characterized as a duopoly. At the same time, competition from onchain prediction markets is intensifying.\n\nLooking ahead, additional entrants are likely, including both traditional operators (i.e., sportsbooks) and crypto-native platforms such as [Hyperliquid](https://x.com/HyperliquidX/status/2018327360723202167) or [Novig](https://messari.io/project/novig/fundraising). Increased competition could pressure Polymarket’s market share, fee structure, and long-term profitability.\n\n### Post-Airdrop Activity Decrease\n\nA portion of Polymarket’s recent activity is likely driven by airdrop farming, though the magnitude is unclear. If a meaningful share of user engagement has been driven by airdrop farming, activity levels, and consequently fee generation, could decline following the distribution event. This creates uncertainty around the durability of current volumes and the sustainability of user growth post-airdrop.\n\n### Market Integrity\n\nMarket integrity remains a critical factor for long-term adoption and credibility. Polymarket’s no-KYC framework, while lowering friction for user participation, may increase the risk of insider trading or information asymmetries. If users perceive that markets are being exploited by participants with privileged information, trust in the platform could erode.\n\nAdditionally, Polymarket relies on UMA’s optimistic oracle for market resolution. Any further high-profile disputes, delays, or controversial resolutions could undermine confidence in the platform’s ability to fairly and accurately settle markets. Repeated incidents may reduce user participation and negatively impact trading volumes over time.\n\n## Conclusion\n\nPolymarket has established itself as a dominant prediction market, generating $31.0 billion in volume, a 31% share, from September 2025 to February 2026. On October 7, 2025, Intercontinental Exchange agreed to invest up to $2 billion at a $9 billion FDV, validating institutional conviction. On March 30, Polymarket extends taker fees to nearly all markets, the most significant step yet toward monetizing its volume. If volume sustains through the fee expansion, Polymarket has a clear path to justifying a premium POLY token valuation.\n\n**Our base case values Polymarket at a $24.2 billion FDV by 2028, with the range spanning $6.4 billion in the bear case to $111.2 billion in the bull case.** The base case is 21% above the sought valuation of $20 billion. The bull case requires fee expansion, volume growth, and fee multiple expansion simultaneously, but the bear case is a reminder that post-TGE volume contraction and fee-driven demand compression are real risks. The most critical variable is volume retention after taker fee expansion, and we urge market participants to track volume across newly fee-charging markets in the 60-90 days following March 30 before drawing firm conclusions about Polymarket’s long-term value.",

"hook": "Valuation of Polymarket's POLY using a ground-up fee multiple framework, with scenario analysis across sports, politics, crypto, and other category volume projections, take rates, and fee multiples.",

"publishDate": "2026-03-26T15:01:00Z",

"readingTimeInMinutes": 32.74666666666667,

"slug": "a-valuation-of-polymarket-poly",

"subscriptionTier": "enterprise",

"summary": "Prediction markets are crypto's latest breakout sector. In February 2026, the sector processed $23.2 billion in monthly volume, up 1,218% year-over-year. Polymarket has led that expansion, generating $31.0 billion in volume and a 31% category share from September 2025 to February 2026. In October 2025, Intercontinental Exchange agreed to invest up to $2 billion at a $9 billion valuation, validating institutional conviction in the platform.\n\nPolymarket operates as a peer-to-peer prediction market across sports, politics, crypto, and other categories, letting users trade directly against each other on a central limit order book. On March 30, Polymarket extends taker fees to nearly all markets, its most significant step toward monetizing the volume it has built. Whether that monetization translates to durable revenue is the central question for POLY investors.\n\nThis report builds a ground-up valuation of Polymarket across market category volume, take rates, and fee multiples to test whether the $20 billion FDV Polymarket was reportedly seeking as of March 7, 2026, is justified by forward fee generation.",

"tags": [

{

"id": "4d0bee6c-b154-42a4-9db2-ed6273808bac",

"name": "Valuations"

},

{

"id": "ddd672c1-e388-472b-8f88-c60f95196e0d",

"name": "Prediction Markets"

}

],

"title": "A Valuation of Polymarket (POLY)",

"previewImage": "https://cdn.sanity.io/images/2bt0j8lu/production/5c9cb3fb8c68658250bdf288ccac0b1636ddc89d-6400x3604.png"

}

}{

"data": "<unknown>",

"error": "<string>"

}{

"data": "<unknown>",

"error": "<string>"

}{

"data": "<unknown>",

"error": "<string>"

}{

"data": "<unknown>",

"error": "<string>"

}Research

Get a research report by report ID

Returns a research report by its report ID

GET

/

research

/

v1

/

reports

/

{reportId}

Get a research report by report ID

curl --request GET \

--url https://api.messari.io/research/v1/reports/{reportId} \

--header 'X-Messari-API-Key: <api-key>'import requests

url = "https://api.messari.io/research/v1/reports/{reportId}"

headers = {"X-Messari-API-Key": "<api-key>"}

response = requests.get(url, headers=headers)

print(response.text)const options = {method: 'GET', headers: {'X-Messari-API-Key': '<api-key>'}};

fetch('https://api.messari.io/research/v1/reports/{reportId}', options)

.then(res => res.json())

.then(res => console.log(res))

.catch(err => console.error(err));<?php

$curl = curl_init();

curl_setopt_array($curl, [

CURLOPT_URL => "https://api.messari.io/research/v1/reports/{reportId}",

CURLOPT_RETURNTRANSFER => true,

CURLOPT_ENCODING => "",

CURLOPT_MAXREDIRS => 10,

CURLOPT_TIMEOUT => 30,

CURLOPT_HTTP_VERSION => CURL_HTTP_VERSION_1_1,

CURLOPT_CUSTOMREQUEST => "GET",

CURLOPT_HTTPHEADER => [

"X-Messari-API-Key: <api-key>"

],

]);

$response = curl_exec($curl);

$err = curl_error($curl);

curl_close($curl);

if ($err) {

echo "cURL Error #:" . $err;

} else {

echo $response;

}package main

import (

"fmt"

"net/http"

"io"

)

func main() {

url := "https://api.messari.io/research/v1/reports/{reportId}"

req, _ := http.NewRequest("GET", url, nil)

req.Header.Add("X-Messari-API-Key", "<api-key>")

res, _ := http.DefaultClient.Do(req)

defer res.Body.Close()

body, _ := io.ReadAll(res.Body)

fmt.Println(string(body))

}HttpResponse<String> response = Unirest.get("https://api.messari.io/research/v1/reports/{reportId}")

.header("X-Messari-API-Key", "<api-key>")

.asString();require 'uri'

require 'net/http'

url = URI("https://api.messari.io/research/v1/reports/{reportId}")

http = Net::HTTP.new(url.host, url.port)

http.use_ssl = true

request = Net::HTTP::Get.new(url)

request["X-Messari-API-Key"] = '<api-key>'

response = http.request(request)

puts response.read_body{

"error": null,

"data": {

"id": "2af98e9e-1c9a-4e31-80be-38e8c1211990",

"createdAt": "2026-03-25T22:43:10Z",

"updatedAt": "2026-03-26T18:17:50Z",

"assetIds": [

"818de6bf-5bb6-42c6-874c-2fb2da81a5b5",

"95111d4e-a862-41e1-829f-d661e1b8f658",

"f8852d39-3261-4345-871e-54d533918dc2",

"99b6a5f4-2200-4098-82fd-53d091bdee70"

],

"assets": [

{

"id": "f8852d39-3261-4345-871e-54d533918dc2",

"name": "Opinion",

"symbol": "opn",

"slug": "opinion"

},

{

"id": "95111d4e-a862-41e1-829f-d661e1b8f658",

"name": "Kalshi",

"symbol": "KALSHI",

"slug": "kalshi"

},

{

"id": "818de6bf-5bb6-42c6-874c-2fb2da81a5b5",

"name": "Polymarket",

"symbol": "POLY",

"slug": "polymarket"

},

{

"id": "99b6a5f4-2200-4098-82fd-53d091bdee70",

"name": "Hyperliquid",

"symbol": "HYPE",

"slug": "hyperliquid"

}

],

"authors": [

{

"id": "ecaf52b1-16eb-4322-bf02-886bea2c5b06",

"name": "Austin Weiler",

"image": "https://cdn.sanity.io/images/2bt0j8lu/production/d70ad0cd21c781575a4fc129c8b634ae0ddd2432-2283x2283.jpg?w=100",

"linkedinUrl": ""

}

],